Summary of Coverage

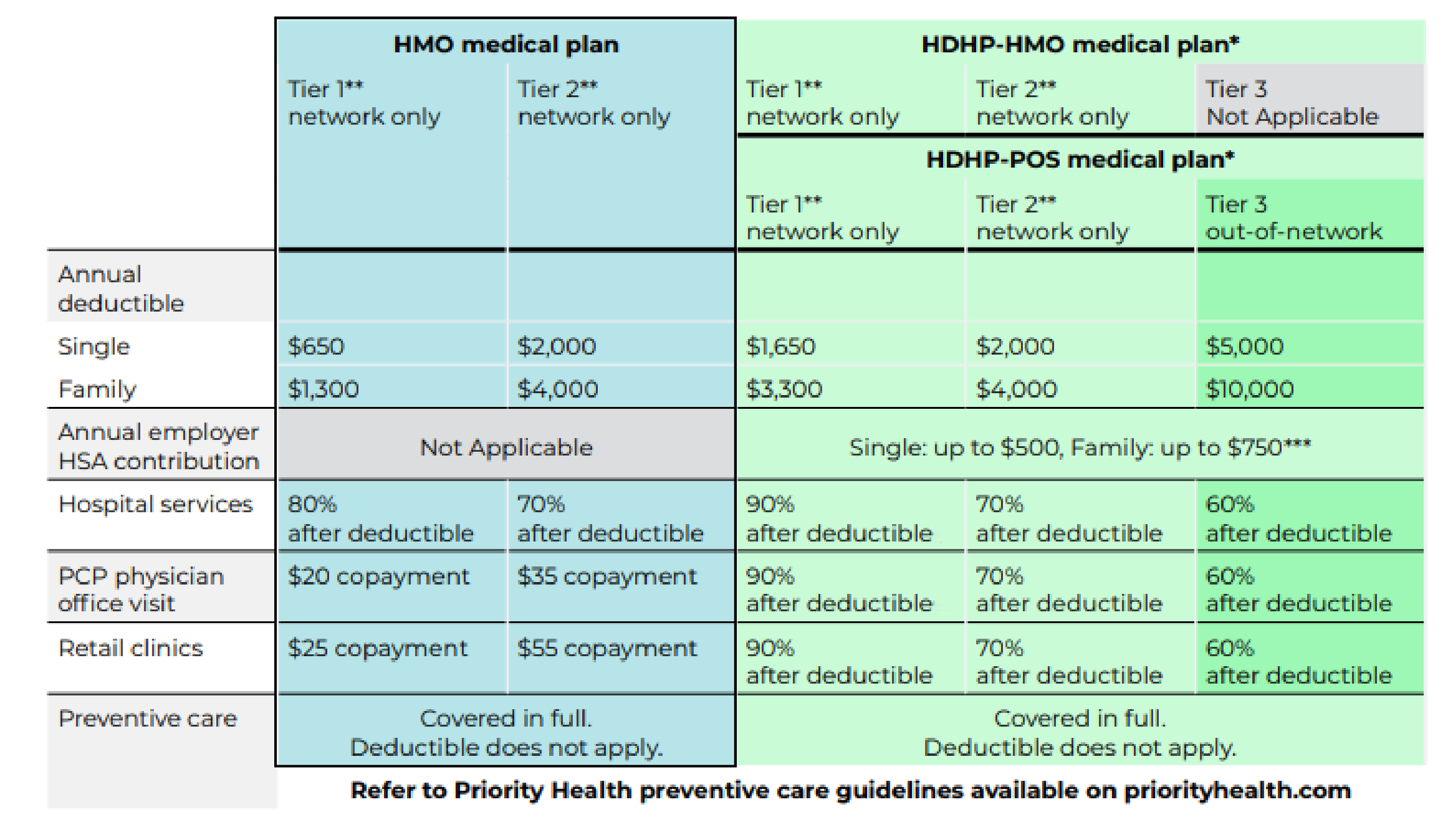

The Health Maintenance Organization (HMO) medical plan covers care provided by in-network providers. With this plan, deductibles are lower, and you share expenses with copayments and co-insurance for all covered services, including prescriptions.

The HMO medical plan covers preventive care, such as yearly physicals, as well as treatment of sickness or injury. The HMO medical plan covers visits to your primary care physician with a copayment. Most inpatient and outpatient services are covered by the plan, with a small portion of coinsurance owed. There is a per-person deductible not to exceed the per-family deductible per contract year.

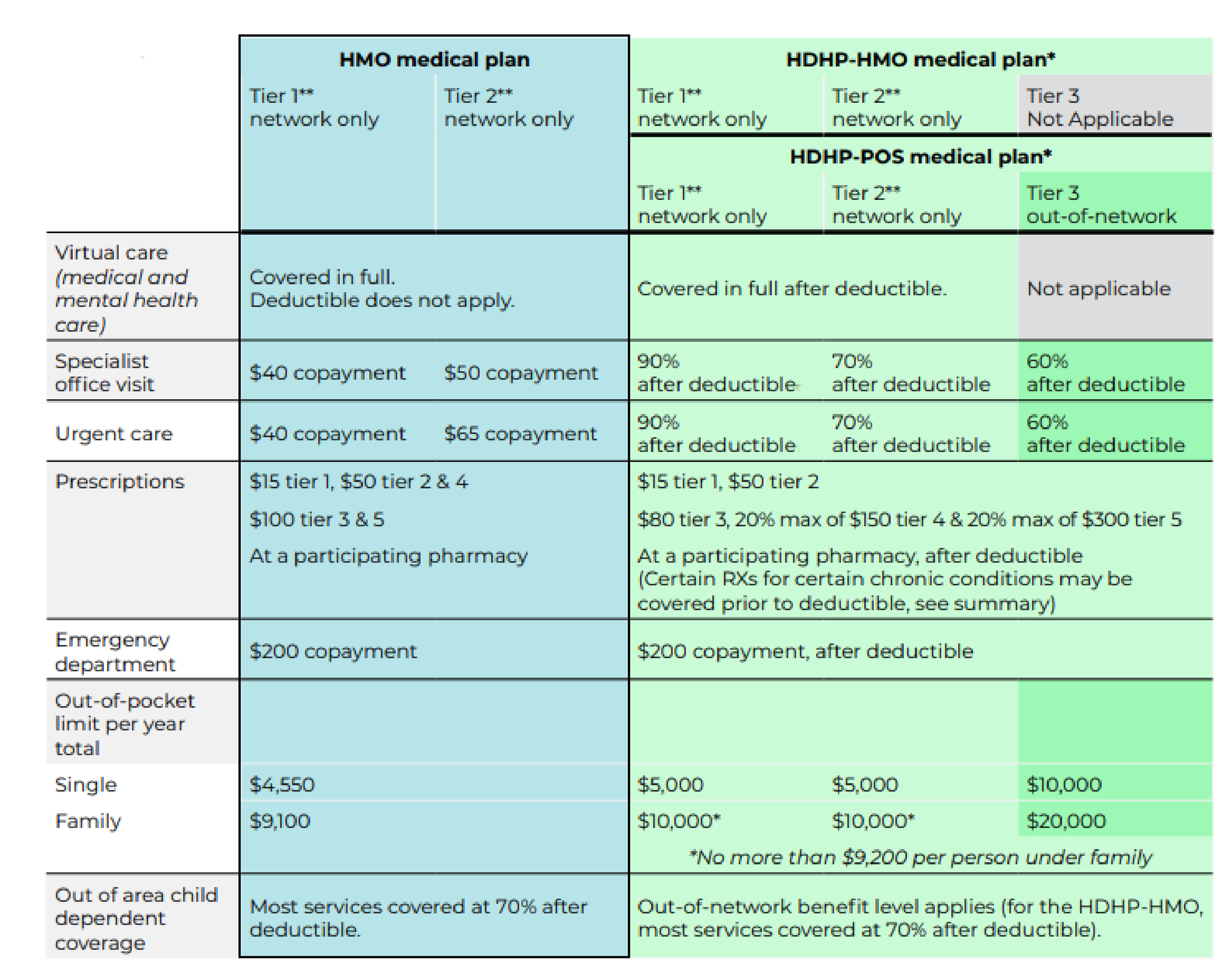

The plan also has an out-of-pocket limit, which will be the most you would pay for services in a calendar year. The out-of-pocket limit includes any deductible, coinsurance, or copayments paid for any covered services and/or prescriptions throughout the year. Once the total limit has been paid, the plan will pay 100 percent for covered services and/or prescriptions.

You must use Priority Health’s (or Cigna if living out of the state of Michigan) participating physicians and facilities to receive benefits, except in an emergency. The plan will not pay benefits if you use a non-participating facility or physician (unless Priority Health has authorized an approved non-participating physician or facility).

*No more than $9,200 per person under family

**For details regarding providers and services for your plan, refer to you benefit guide.

***Annual Corewell Health employer HSA contribution is deposited into the HSA account each paycheck (approx. $19.23 per pay for single and $28.75 per pay for all other coverage tiers until the maximum has been reached).

Tier 2 services that apply to the deductible will credit both Tier 1 and Tier 2 deductibles. Only Tier 1 services will credit Tier 1 deductibles. Tier 1 and Tier 2 out-of-pocket maximums track in combination. On the HDHP-POS plan Tier 3 does not apply to Tier 1 or Tier 2. The HDHP-HMO plan provides a similar network as the HMO plan and does not include coverage for out of network providers.

How your plan pays for care:

You Pay:

Copays or provider bills until you reach the deductible.

- If a service does not have a copay, such as hospitalization or hospitalization services, you pay the provider bill.

- In the HMO plan, each person on the plan can meet an individual deductible.

- Tier 2 services that apply to the deductible will credit both Tier 1 and Tier 2 deductibles. Only Tier 1 services will credit Tier 1 deductibles. Tier 1 and Tier 2 out-of-pocket maximums track in combination.

You + The Plan Pay:

- Once you have paid the deductible, the plan will share the cost of the remaining expenses through co-insurance, until you have reached the out-of-pocket limit.

- The out-of-pocket limit is the limit of all of your costs for the year. Deductibles, co-insurance and copays all apply to the out-of-pocket limit.

- Costs are higher outside of Tier 1 providers: your share of the bill, the deductible, and the out-of-pocket maximum all increase in the Tier 2 network.

The Plan Pays:

- Most costs above the out-of-pocket limit. The plan covers 100% of eligible costs (such as coinsurance) for the rest of the year.

ServiceNow keyword: hmo plan